- Home

- IIA Certifications

- IIA-CIA-Part2 Certified Internal Auditor - Part 2, Practice of Internal Auditing Dumps

Pass IIA IIA-CIA-Part2 Exam in First Attempt Guaranteed!

Get 100% Latest Exam Questions, Accurate & Verified Answers to Pass the Actual Exam!

30 Days Free Updates, Instant Download!

IIA-CIA-Part2 Premium Bundle

- Premium File 956 Questions & Answers. Last update: Jul 28, 2026

- Training Course 93 Video Lectures

- Study Guide 438 Pages

Last Week Results!

Includes question types found on the actual exam such as drag and drop, simulation, type-in and fill-in-the-blank.

Based on real-life scenarios similar to those encountered in the exam, allowing you to learn by working with real equipment.

Developed by IT experts who have passed the exam in the past. Covers in-depth knowledge required for exam preparation.

All IIA IIA-CIA-Part2 certification exam dumps, study guide, training courses are Prepared by industry experts. PrepAway's ETE files povide the IIA-CIA-Part2 Certified Internal Auditor - Part 2, Practice of Internal Auditing practice test questions and answers & exam dumps, study guide and training courses help you study and pass hassle-free!

CIA Exam Part 2 Made Simple: How to Pass with Confidence

CIA Part 2 focuses on the practical aspects of internal auditing, emphasizing the skills and knowledge required to plan, execute, and report on audit engagements. This part of the exam evaluates a candidate’s ability to manage the internal audit activity, perform audit engagements effectively, and communicate findings to stakeholders. Understanding the structure and purpose of this exam part is essential for professional growth in internal auditing.

Managing the Internal Audit Activity

Managing the internal audit activity is a critical component of this exam. Candidates must understand how to establish a risk-based internal audit plan that aligns with organizational objectives and priorities. This includes identifying high-risk areas, allocating resources efficiently, and monitoring audit activities to ensure they meet performance standards.

Effective management involves overseeing audit teams, coordinating assignments, and maintaining professional standards throughout the engagement lifecycle. Auditors are expected to provide guidance, review workpapers, and ensure that audits are conducted in accordance with internal auditing frameworks. Communication with senior management and governance bodies is also essential, providing insight into risk exposure, control effectiveness, and operational efficiency.

Planning the Engagement

Engagement planning sets the foundation for a successful audit. Candidates are required to demonstrate proficiency in defining audit objectives, determining scope, and selecting appropriate procedures. Planning involves evaluating organizational risks, understanding operational processes, and identifying key control points.

Auditors must consider materiality, regulatory requirements, and potential operational vulnerabilities when designing an engagement plan. Developing a structured plan ensures that resources are used effectively, high-risk areas are prioritized, and audit procedures are conducted systematically. Planning also includes coordinating with relevant departments, scheduling fieldwork, and anticipating challenges that may arise during the audit process.

Performing the Engagement

Performing an audit engagement requires practical application of internal audit techniques to gather evidence, evaluate controls, and analyze operational performance. Candidates must understand various methods for collecting and assessing information, including reviewing documents, observing processes, conducting interviews, and performing analytical testing.

Auditors evaluate whether internal controls are properly designed and operating effectively. They assess compliance with organizational policies, regulatory requirements, and professional standards. The process includes identifying weaknesses, operational inefficiencies, and areas for improvement. Candidates must also demonstrate professional skepticism, ensuring that conclusions are supported by reliable evidence and that recommendations are practical and actionable.

Information Gathering and Evidence Evaluation

Information gathering is a central component of performing an audit. Candidates are expected to collect relevant data, analyze it, and interpret findings in the context of organizational objectives. This involves assessing the sufficiency, relevance, and reliability of evidence to support audit conclusions.

Techniques for evidence evaluation include examining documentation, performing sampling tests, conducting walkthroughs, and using analytical procedures. Auditors must identify trends, anomalies, or discrepancies that may indicate control deficiencies or operational risks. Evaluating evidence effectively requires critical thinking, attention to detail, and an understanding of internal audit standards and frameworks.

Communicating Engagement Results

Communicating audit results is essential for ensuring that findings are understood and acted upon by management and governance bodies. Candidates must demonstrate the ability to prepare clear, concise, and informative reports that highlight key risks, control deficiencies, and recommended actions.

Reports should be structured to provide insight into the implications of findings, prioritize risks, and suggest practical solutions. Effective communication also involves discussing results with relevant stakeholders, clarifying issues, and addressing questions or concerns. Auditors must present information objectively and professionally, ensuring that recommendations are actionable and aligned with organizational objectives.

Monitoring and Follow-Up

Monitoring and follow-up activities ensure that audit recommendations are implemented and controls are improved. Candidates must understand how to track corrective actions, assess their effectiveness, and report progress to management and governance bodies. Continuous monitoring reinforces accountability, supports risk management, and contributes to ongoing operational improvement.

Auditors evaluate whether implemented actions have adequately addressed identified risks and whether additional measures are necessary. Effective follow-up ensures that recommendations result in tangible improvements, strengthens internal controls, and enhances organizational performance.

Cognitive Levels and Skill Requirements

The exam tests candidates at two cognitive levels: basic and proficient. The basic level requires recall of relevant concepts and understanding of fundamental processes. The proficient level emphasizes application, analysis, evaluation, and judgment. Candidates must demonstrate the ability to integrate knowledge across multiple areas, apply auditing standards, and make informed decisions based on evidence.

Mastery of both cognitive levels ensures that auditors can handle a range of scenarios, from straightforward control assessments to complex operational evaluations. Proficient-level understanding is essential for evaluating audit findings, recommending improvements, and providing strategic insights to management.

Exam Structure and Question Format

CIA Part 2 consists of multiple-choice questions designed to assess practical knowledge and applied skills. The exam includes scenarios that simulate real-world audit situations, requiring candidates to evaluate processes, analyze risks, and determine appropriate actions. Time management is critical, as candidates must complete all questions within the allotted period while applying professional judgment effectively.

Candidates are expected to demonstrate both theoretical understanding and the ability to apply knowledge in practical contexts. Familiarity with internal audit standards, procedures, and best practices is essential for navigating the question format successfully.

Importance of Practical Experience

Practical experience in internal auditing provides candidates with an advantage in understanding the exam content. Exposure to real-world audit activities, risk assessments, and control evaluations helps candidates relate theoretical concepts to practical applications. This experience enhances comprehension of engagement planning, evidence gathering, and reporting processes, enabling candidates to perform effectively under exam conditions.

Understanding the operational context of auditing allows candidates to anticipate challenges, interpret scenarios accurately, and apply professional judgment in evaluating risks and controls. Candidates without extensive experience may need to focus more on understanding practical applications and scenario-based exercises.

Key Areas of Focus for Study

Candidates should focus on mastering the internal audit process, including managing audit functions, planning engagements, performing fieldwork, gathering evidence, evaluating controls, reporting results, and monitoring outcomes. Understanding the relationship between risk assessment and control evaluation is crucial for effective auditing.

Proficiency in applying professional standards, interpreting operational data, and formulating actionable recommendations ensures that candidates can perform audits that add value to an organization. Familiarity with engagement techniques, documentation practices, and communication methods is also essential for exam success.

Strategic Importance of Internal Auditing

Internal auditing plays a strategic role by supporting governance, enhancing operational efficiency, and mitigating organizational risks. Candidates must understand how audit activities provide insight into business processes, influence decision-making, and contribute to organizational objectives. Recognizing this strategic value helps candidates appreciate the purpose behind audit procedures and reinforces the importance of professional standards.

Applying Knowledge in Scenario-Based Contexts

CIA Part 2 emphasizes applying auditing knowledge in practical, scenario-based contexts. Candidates are tested on their ability to analyze situations, identify risks, evaluate control effectiveness, and provide actionable recommendations. Scenario-based exercises develop critical thinking, problem-solving, and professional judgment skills.

Candidates must integrate information from multiple sources, consider operational and regulatory implications, and prioritize actions based on risk assessment. Effective application of knowledge in these scenarios demonstrates readiness to conduct real-world audits and contributes to professional competence.

Quality Assurance and Audit Effectiveness

Maintaining high-quality audits is essential for credibility and effectiveness. Candidates must understand quality assurance practices, including peer review, supervisory checks, and adherence to internal audit standards. High-quality audits produce reliable findings, support governance, and enhance stakeholder confidence.

Auditors assess the sufficiency of evidence, the clarity of reporting, and the practicality of recommendations. Continuous evaluation of audit effectiveness ensures that processes are improved over time, controls are strengthened, and organizational objectives are supported.

Professional Judgment and Decision-Making

Professional judgment is a core competency for internal auditors. Candidates are required to apply judgment in planning engagements, evaluating evidence, assessing risks, and communicating findings. The ability to make informed decisions ensures that audits are thorough, accurate, and aligned with organizational priorities.

Judgment is applied when interpreting complex scenarios, balancing competing priorities, and selecting appropriate audit procedures. Strong judgment skills enable auditors to provide practical recommendations, anticipate potential issues, and address operational challenges effectively.

Integration of Technology in Auditing

Modern auditing increasingly relies on technology to enhance efficiency and accuracy. Candidates should understand how tools such as data analytics, automated testing, and continuous monitoring support audit activities. Technology enables auditors to process large volumes of information, identify anomalies, and evaluate controls more effectively.

Integration of technology allows auditors to provide deeper insights, improve accuracy, and streamline reporting. Candidates must demonstrate the ability to apply technological tools appropriately, interpret results, and incorporate findings into audit conclusions and recommendations.

Preparing for Proficient-Level Topics

Proficient-level topics require candidates to analyze, evaluate, and synthesize information. This includes assessing complex control systems, interpreting operational data, and formulating recommendations that are practical and actionable. Mastery of these topics ensures candidates can handle real-world audit challenges and provide meaningful contributions to organizational performance.

Study approaches should emphasize scenario-based exercises, application of professional standards, and critical evaluation of internal controls. Developing proficiency in these areas reinforces understanding of audit processes and prepares candidates for practical auditing responsibilities.

Time Management and Exam Readiness

Effective time management is essential for completing the CIA Part 2 exam. Candidates must allocate sufficient time to read scenarios, analyze information, and select the best answers within the time limit. Practicing under timed conditions helps build confidence, accuracy, and efficiency.

Readiness also involves reviewing key concepts, understanding cognitive requirements, and practicing the application of knowledge in realistic scenarios. Candidates should evaluate their strengths and weaknesses to focus study efforts on areas requiring improvement.

CIA Part 2 emphasizes practical internal auditing skills, including managing audit activities, planning and performing engagements, evaluating evidence, reporting findings, and monitoring outcomes. The exam assesses both basic and proficient levels of knowledge, requiring candidates to apply standards, professional judgment, and analytical skills.

Thorough preparation, scenario-based practice, and understanding of internal audit procedures are critical for success. Candidates who integrate theoretical knowledge with practical application, maintain quality in their audits, and demonstrate professional judgment are well-positioned to excel in CIA Part 2 and in professional auditing roles

Understanding the Role of Internal Audit in Organizations

Internal auditing serves as a key function in ensuring that organizational objectives are achieved efficiently, risks are managed effectively, and governance structures are strengthened. The CIA Part 2 exam emphasizes the practical application of internal auditing principles, focusing on how auditors plan, execute, and communicate audit activities. Candidates are expected to demonstrate an understanding of how internal audits support operational effectiveness, regulatory compliance, and strategic decision-making.

Auditors must recognize the broader impact of their work, including how audit findings can influence management decisions and improve business processes. Understanding the strategic role of internal auditing helps candidates approach audit engagements with a holistic perspective, integrating risk assessment, process evaluation, and control analysis.

Establishing a Risk-Based Internal Audit Plan

Developing a risk-based internal audit plan is a central aspect of CIA Part 2. Candidates must understand how to identify organizational risks, assess their potential impact, and prioritize audit activities accordingly. This involves evaluating operational, financial, and compliance risks, and aligning the audit schedule with areas of greatest concern.

The process requires coordination with senior management and governance bodies to ensure that audit objectives align with organizational priorities. Auditors must also account for available resources, timelines, and the complexity of operations. A well-structured plan ensures that audits are conducted efficiently and that critical risks are addressed systematically.

Structuring Audit Engagements

Planning individual audit engagements involves defining the scope, objectives, and methodology for assessing processes and controls. Candidates must demonstrate knowledge of how to design engagement procedures that effectively gather evidence and assess operational performance.

Engagement planning includes understanding key business processes, identifying relevant control points, and determining the appropriate testing techniques. Auditors must also anticipate challenges, ensure compliance with professional standards, and establish a framework for documenting findings. Proper engagement planning facilitates accurate evaluation and ensures that audit conclusions are well-supported.

Techniques for Evidence Collection

Evidence collection is a critical part of performing an audit. CIA Part 2 tests candidates on their ability to apply various methods for gathering information, including reviewing documents, observing procedures, conducting interviews, and performing analytical assessments.

Candidates must evaluate the relevance, sufficiency, and reliability of evidence to support audit findings. Analytical techniques, such as variance analysis, trend evaluation, and control testing, help auditors identify weaknesses, inefficiencies, and potential areas of risk. The ability to collect and interpret evidence effectively ensures that conclusions are accurate and actionable.

Evaluating Internal Controls

Evaluating internal controls requires an understanding of their design, implementation, and operational effectiveness. Candidates are expected to assess whether controls mitigate identified risks and whether gaps exist that could affect organizational objectives.

Auditors must consider control objectives, regulatory requirements, and process efficiency when evaluating control effectiveness. This involves testing transactions, reviewing procedures, and determining whether controls are applied consistently. Evaluating internal controls allows auditors to provide recommendations that strengthen operational integrity and support risk management initiatives.

Performing Analytical Procedures

Analytical procedures assist auditors in identifying patterns, trends, and anomalies that may indicate control deficiencies or operational inefficiencies. CIA Part 2 examines candidates’ ability to apply analytical techniques to assess financial and operational data.

Candidates must interpret results, compare actual performance with expected outcomes, and investigate deviations that could signal risks or errors. Effective analytical skills enable auditors to focus on critical areas, allocate resources efficiently, and provide management with valuable insights for decision-making.

Communicating Findings and Recommendations

Clear and effective communication of audit findings is essential for ensuring that recommendations are understood and implemented. Candidates are expected to prepare reports that summarize key risks, highlight control weaknesses, and propose actionable solutions.

Auditors must tailor their communication to the audience, ensuring that management and governance bodies can comprehend the implications of findings. Effective reporting also involves prioritizing issues based on risk severity, presenting evidence logically, and offering practical recommendations that enhance operational effectiveness.

Monitoring and Follow-Up Activities

Follow-up is an integral part of the internal audit process. CIA Part 2 emphasizes the importance of tracking the implementation of recommendations, assessing the effectiveness of corrective actions, and reporting progress to management.

Auditors evaluate whether actions address identified risks, improve control effectiveness, and contribute to organizational performance. Continuous monitoring ensures accountability and supports ongoing improvement, reinforcing the value of the internal audit function.

Applying Professional Standards

Candidates must demonstrate knowledge of professional internal auditing standards, including those related to engagement planning, evidence collection, reporting, and monitoring. CIA Part 2 examines the ability to apply these standards in practical scenarios, ensuring that audits are conducted systematically and ethically.

Adherence to standards guides the auditor’s approach, ensures consistency in evaluations, and enhances the credibility of findings. Candidates are expected to integrate standards with practical judgment to provide meaningful insights that support organizational objectives.

Scenario-Based Application of Knowledge

CIA Part 2 emphasizes applying theoretical knowledge to real-world scenarios. Candidates must analyze complex situations, identify risks, evaluate controls, and recommend appropriate actions. Scenario-based questions test critical thinking, decision-making, and professional judgment.

Applying knowledge in practical contexts requires synthesizing information from multiple sources, considering operational and regulatory implications, and prioritizing actions based on risk assessment. This approach prepares auditors to address real-world challenges effectively and enhances their ability to make informed recommendations.

Quality Assurance in Auditing

Ensuring audit quality is essential for credibility and effectiveness. Candidates must understand quality assurance practices, including supervisory reviews, peer assessments, and adherence to internal audit standards. High-quality audits provide reliable findings, support governance, and reinforce stakeholder confidence.

Auditors must assess the sufficiency of evidence, the clarity of reporting, and the practicality of recommendations. Continuous evaluation and improvement of audit processes strengthen controls and enhance organizational performance.

Professional Judgment and Decision-Making

Professional judgment is fundamental in internal auditing. CIA Part 2 examines candidates’ ability to apply judgment when planning engagements, evaluating evidence, assessing risks, and communicating findings. Effective decision-making ensures audits are thorough, accurate, and aligned with organizational priorities.

Auditors use judgment to interpret complex information, weigh competing priorities, and determine the most appropriate procedures. Strong professional judgment enhances the quality of recommendations, supports effective risk management, and improves operational outcomes.

Technology in Internal Auditing

The integration of technology in auditing improves efficiency, accuracy, and insight. Candidates should understand how tools such as data analytics, automated testing, and continuous monitoring support audit activities. CIA Part 2 tests the ability to leverage technology to analyze information, identify anomalies, and evaluate control effectiveness.

Effective use of technology allows auditors to process large volumes of data, detect patterns, and enhance the reliability of findings. Candidates must demonstrate the ability to interpret technological outputs and integrate them into audit conclusions and recommendations.

Risk Assessment and Control Evaluation

Understanding the relationship between risk and controls is central to internal auditing. Candidates must evaluate how controls mitigate identified risks and assess whether gaps exist that could compromise objectives. CIA Part 2 emphasizes applying risk assessment principles to prioritize audit activities and focus on areas of greatest impact.

Auditors must integrate risk and control evaluation to ensure that audits provide meaningful insights and support organizational governance. This requires analyzing processes, testing control effectiveness, and recommending improvements that enhance operational integrity.

Continuous Improvement in Audit Practice

CIA Part 2 highlights the role of internal auditing in continuous organizational improvement. Candidates should understand how audits identify inefficiencies, promote best practices, and contribute to operational excellence. Auditors evaluate processes, recommend enhancements, and monitor implementation to ensure lasting impact.

Continuous improvement involves reviewing audit approaches, updating procedures, and adapting to changes in organizational structure, technology, and regulatory requirements. Auditors play a proactive role in enhancing processes and supporting strategic goals.

Preparing for Proficient-Level Topics

Proficient-level topics in CIA Part 2 require analysis, evaluation, and synthesis of information. Candidates must assess complex control systems, interpret operational data, and formulate actionable recommendations. Mastery of these areas ensures readiness to handle real-world audit challenges effectively.

Study approaches should include scenario-based exercises, critical evaluation of controls, and application of professional standards. Proficiency in these topics reinforces practical auditing skills and prepares candidates for responsibilities in professional internal audit roles.

Study Strategies for CIA Part 2

Successful preparation involves structured study, consistent review, and application of knowledge in practical contexts. Candidates should allocate sufficient time to understand internal audit principles, professional standards, and engagement processes. Practice exercises help reinforce learning, improve problem-solving skills, and enhance time management.

Scenario-based study is particularly effective, allowing candidates to simulate audit engagements, evaluate risks, and formulate recommendations. Regular assessment of understanding ensures that knowledge is retained and can be applied effectively during the exam.

Exam Readiness and Time Management

Effective time management is critical for completing all questions within the exam duration. Candidates should practice under timed conditions to build efficiency and accuracy. Evaluating readiness involves assessing strengths and weaknesses, focusing study efforts on areas requiring improvement, and practicing the application of concepts in realistic scenarios.

Confidence in understanding the internal audit process, professional standards, and engagement procedures contributes to performance during the exam. Candidates must integrate theoretical knowledge with practical application to respond effectively to scenario-based questions.

CIA Part 2 evaluates candidates on practical internal auditing skills, including managing audit activities, planning and performing engagements, evaluating evidence, reporting findings, and monitoring outcomes. The exam tests both basic and proficient knowledge, emphasizing the application of professional standards, analytical skills, and judgment.

Thorough preparation, scenario-based practice, and understanding of internal auditing processes are essential for success. Candidates who integrate theoretical concepts with practical application, maintain quality in audits, and demonstrate professional judgment are well-positioned to excel in CIA Part 2 and contribute effectively in professional internal audit roles

The Purpose of CIA Part 2

CIA Part 2 focuses on the practice of internal auditing, assessing a candidate’s ability to plan, execute, and communicate audit engagements effectively. This part of the exam emphasizes practical application of internal auditing standards, risk management, and process evaluation. Understanding the purpose and scope of this exam is essential for demonstrating competence in professional auditing roles.

Internal auditing provides organizations with insight into risk exposures, operational efficiency, and governance processes. Candidates must be able to apply knowledge to real-world scenarios, identifying control weaknesses, evaluating processes, and recommending improvements. This exam part tests not only theoretical understanding but also the ability to analyze, interpret, and act upon audit information effectively.

Risk-Based Internal Audit Planning

A key focus of CIA Part 2 is risk-based audit planning. Candidates must demonstrate the ability to identify high-risk areas, prioritize engagements, and allocate resources efficiently. This requires understanding organizational objectives, operational risks, and regulatory requirements.

Effective planning includes defining the scope of audits, setting objectives, and selecting appropriate audit techniques. Auditors must anticipate challenges, coordinate with stakeholders, and ensure that engagements address critical areas. Planning serves as a foundation for all subsequent audit activities, ensuring that resources are used effectively and audit goals are achieved.

Engagement Execution

Executing an audit engagement involves collecting evidence, evaluating controls, and performing analytical procedures. Candidates must understand how to gather relevant data, assess the reliability of information, and analyze operational effectiveness.

Auditors apply techniques such as document review, process observation, interviews, and data analysis to assess controls and operational performance. Evaluating evidence requires critical thinking, attention to detail, and adherence to professional standards. Findings must be substantiated and presented logically to support actionable recommendations.

Control Assessment and Evaluation

Control assessment is central to CIA Part 2. Candidates are expected to evaluate whether controls are designed effectively and operating as intended. This includes reviewing financial and operational processes, identifying gaps, and determining the potential impact of deficiencies.

Auditors must consider internal policies, regulatory requirements, and risk exposures when evaluating controls. Proper assessment ensures that audit findings provide meaningful insight into organizational performance and risk mitigation. Effective control evaluation helps organizations strengthen processes, enhance accountability, and support governance objectives.

Analytical Procedures in Auditing

Analytical procedures are used to identify trends, anomalies, and deviations in operational and financial data. CIA Part 2 emphasizes the application of analytical techniques to detect potential risks and inefficiencies.

Candidates must interpret data, compare actual performance against benchmarks, and investigate irregularities. Analytical skills allow auditors to focus on critical areas, allocate resources effectively, and provide management with actionable insights. These procedures support evidence-based conclusions and enhance the credibility of audit findings.

Reporting and Communication

Clear communication of audit results is essential for ensuring that recommendations are understood and implemented. Candidates must demonstrate the ability to prepare reports that summarize key findings, highlight risks, and propose practical solutions.

Effective reporting involves structuring information logically, prioritizing issues, and tailoring communication to stakeholders. Auditors must present findings objectively, support recommendations with evidence, and ensure that management understands the implications of audit results. Communication skills are vital for influencing decisions and driving improvements within the organization.

Follow-Up and Monitoring

Monitoring and follow-up activities ensure that audit recommendations are implemented and controls are strengthened. Candidates must understand how to track corrective actions, assess their effectiveness, and report progress to management and governance bodies.

Continuous monitoring reinforces accountability, supports risk management, and contributes to operational improvement. Auditors must evaluate whether implemented actions adequately address identified risks and whether additional measures are required. Follow-up ensures that audit activities have a lasting impact on organizational performance.

Cognitive Skills Tested

CIA Part 2 assesses candidates at basic and proficient cognitive levels. Basic-level questions require recall of relevant concepts and understanding of fundamental processes. Proficient-level questions test the application of knowledge, analysis, evaluation, and judgment.

Candidates must integrate knowledge from multiple areas, apply standards, and make informed decisions. Mastery of both cognitive levels demonstrates readiness to perform professional audit tasks, evaluate complex situations, and provide actionable recommendations.

Scenario-Based Applications

Scenario-based questions are a significant part of CIA Part 2. Candidates are tested on their ability to analyze situations, identify risks, evaluate controls, and propose solutions. These scenarios simulate real-world challenges auditors face, requiring critical thinking and professional judgment.

Application of knowledge in practical contexts involves synthesizing information, prioritizing risks, and selecting appropriate audit procedures. Candidates must demonstrate the ability to interpret scenarios accurately, apply standards effectively, and provide actionable recommendations.

Professional Standards in Practice

Knowledge and application of professional standards are essential for success in CIA Part 2. Candidates must understand standards related to audit planning, evidence collection, reporting, and follow-up. Applying standards ensures that audit activities are conducted systematically, ethically, and in alignment with best practices.

Adherence to standards enhances credibility, supports governance, and ensures consistent evaluation of controls and processes. Candidates must integrate professional standards with practical judgment to deliver meaningful audit findings and recommendations.

Integration of Technology

Modern internal auditing increasingly relies on technology to enhance efficiency and accuracy. CIA Part 2 tests candidates’ understanding of tools such as data analytics, automated testing, and continuous monitoring.

Technology supports auditors in processing large volumes of information, detecting patterns, and evaluating controls effectively. Candidates must demonstrate the ability to interpret technological outputs, integrate results into audit conclusions, and use technology to enhance the overall audit process.

Risk Assessment and Prioritization

Understanding risk assessment is crucial for prioritizing audit engagements. Candidates must evaluate the likelihood and impact of risks, determine areas requiring attention, and focus resources accordingly. CIA Part 2 emphasizes the application of risk assessment principles to ensure that audit activities address the most critical organizational concerns.

Effective prioritization allows auditors to target high-risk areas, allocate resources efficiently, and provide management with insights that enhance decision-making. Candidates must demonstrate the ability to balance operational priorities, regulatory requirements, and organizational objectives in planning and executing audits.

Enhancing Operational Effectiveness

Audits aim to improve organizational efficiency and effectiveness. CIA Part 2 emphasizes evaluating operational processes, identifying inefficiencies, and recommending improvements. Candidates must demonstrate the ability to provide actionable recommendations that strengthen processes, enhance controls, and support organizational goals.

Auditors contribute to continuous improvement by analyzing performance metrics, assessing workflows, and identifying opportunities for optimization. Effective audits ensure that processes operate efficiently, risks are mitigated, and resources are utilized effectively.

Professional Judgment and Decision-Making

Professional judgment is essential in audit planning, evidence evaluation, risk assessment, and reporting. Candidates must demonstrate the ability to make informed decisions based on available information and professional standards.

Judgment is applied in evaluating complex situations, balancing competing priorities, and selecting appropriate procedures. Strong judgment skills allow auditors to provide recommendations that are practical, effective, and aligned with organizational objectives.

Preparing for Proficient-Level Topics

Proficient-level topics require candidates to analyze complex processes, evaluate control systems, and formulate actionable recommendations. CIA Part 2 emphasizes higher-order thinking, including synthesis, evaluation, and professional judgment.

Preparation involves scenario-based exercises, critical review of audit standards, and application of analytical techniques. Developing proficiency ensures that candidates can address real-world challenges and contribute meaningfully to organizational audit activities.

Time Management and Exam Strategy

Completing the exam within the allocated time is essential. CIA Part 2 candidates must practice reading scenarios, analyzing data, and selecting appropriate responses efficiently. Timed practice helps build accuracy, confidence, and stamina for answering all questions.

Strategic study involves reviewing key concepts, practicing scenario-based applications, and reinforcing professional standards. Candidates must assess readiness, focus on weaker areas, and ensure that they can apply knowledge effectively under exam conditions.

Continuous Learning in Internal Auditing

Continuous learning enhances the auditor’s ability to adapt to evolving organizational risks, standards, and technologies. CIA Part 2 emphasizes understanding current practices, applying professional standards, and integrating emerging tools to improve audit effectiveness.

Auditors must stay informed about changes in governance, risk management, and operational practices. Continuous learning supports professional growth, strengthens audit quality, and ensures that audit activities remain relevant and impactful.

Practical Application of Concepts

CIA Part 2 requires candidates to translate theoretical knowledge into practical auditing skills. This involves planning and executing engagements, evaluating risks and controls, analyzing information, and providing actionable recommendations.

Practical application develops critical thinking, problem-solving, and decision-making skills. Candidates must integrate knowledge from multiple areas, consider operational and regulatory implications, and apply professional judgment to deliver meaningful audit outcomes.

Reporting and Follow-Up Best Practices

Effective reporting and follow-up ensure that audit recommendations lead to tangible improvements. Candidates must understand how to track corrective actions, assess their impact, and communicate progress to management.

Auditors should prioritize recommendations based on risk, provide clear and concise reports, and monitor implementation to ensure long-term benefits. Follow-up activities reinforce accountability and demonstrate the value of the internal audit function.

Strategic Impact of Internal Auditing

Internal auditing contributes to organizational governance, risk management, and operational improvement. CIA Part 2 emphasizes understanding how audit activities influence decision-making, mitigate risks, and enhance process efficiency.

Candidates must recognize the broader organizational context, ensuring that audit activities align with strategic objectives and support continuous improvement. This perspective helps auditors provide insights that strengthen performance and governance practices.

CIA Part 2 evaluates practical auditing skills, including planning, performing, and reporting audit engagements. The exam tests knowledge at basic and proficient levels, emphasizing professional standards, risk assessment, analytical skills, and judgment.

Thorough preparation, scenario-based practice, and understanding of internal audit processes are critical for success. Candidates who integrate theoretical knowledge with practical application, maintain audit quality, and demonstrate professional judgment are well-prepared to excel in CIA Part 2 and contribute effectively to organizational audit activities

Understanding the Scope of CIA Part 2

CIA Part 2 centers on the practice of internal auditing, examining a candidate’s ability to plan, conduct, and report audit engagements effectively. This section of the exam evaluates practical knowledge, analytical skills, and professional judgment required for performing internal audit functions. Candidates are expected to demonstrate proficiency in applying auditing standards, assessing risk, evaluating controls, and providing actionable recommendations.

The exam emphasizes how internal auditing supports organizational goals by improving operational efficiency, mitigating risks, and strengthening governance. Candidates must understand the strategic value of audit activities and how audit findings can influence decision-making across various operational and financial processes.

Managing the Internal Audit Activity

Candidates must grasp how to manage the internal audit function within an organization. This includes establishing audit policies, defining objectives, and coordinating with governance bodies to align audit activities with organizational priorities. Understanding resource allocation, risk-based audit scheduling, and audit team management is essential for ensuring effective internal audit operations.

Management responsibilities include overseeing engagement execution, ensuring adherence to standards, and fostering a culture of accountability. Proper oversight ensures that audits are conducted efficiently, findings are reliable, and recommendations are implemented to strengthen control and governance frameworks.

Engagement Planning Fundamentals

Planning individual audit engagements is a critical focus of CIA Part 2. Candidates should understand how to define the scope, objectives, and methodology for each engagement. Planning requires identification of key processes, potential risks, and relevant controls, as well as determining the procedures needed to gather sufficient and reliable evidence.

Effective engagement planning ensures that audit efforts are targeted, resources are optimized, and high-risk areas are prioritized. Candidates must demonstrate the ability to anticipate challenges, establish testing approaches, and coordinate with relevant stakeholders to execute audits effectively.

Gathering and Evaluating Evidence

Performing an audit engagement involves collecting and evaluating evidence to assess organizational processes and controls. Candidates must understand the appropriate techniques for evidence collection, including reviewing documentation, observing procedures, conducting interviews, and performing analytical procedures.

Evaluating evidence requires assessing its relevance, reliability, and sufficiency to support audit conclusions. Analytical skills, such as trend analysis, variance review, and control testing, help auditors identify weaknesses, inefficiencies, and operational risks. Sound evidence collection and evaluation ensure that audit findings are accurate, meaningful, and actionable.

Assessing Internal Controls

Internal control assessment is a cornerstone of CIA Part 2. Candidates are expected to evaluate whether controls are designed effectively and operating as intended. This involves reviewing financial, operational, and compliance processes to identify gaps or deficiencies.

Auditors must consider organizational policies, risk exposures, and regulatory requirements when assessing controls. Proper evaluation allows auditors to provide recommendations that strengthen processes, mitigate risks, and enhance organizational accountability. Understanding how controls interact with operational objectives is key to making informed audit decisions.

Applying Analytical Techniques

Analytical procedures are used to detect deviations, trends, or anomalies that may indicate risk exposure or control weaknesses. CIA Part 2 tests candidates’ ability to analyze data, identify patterns, and interpret findings to inform audit conclusions.

Candidates must compare actual performance against expectations, investigate discrepancies, and prioritize audit attention based on risk significance. Effective application of analytical techniques allows auditors to focus on critical areas, allocate resources efficiently, and provide evidence-based recommendations that improve operations and mitigate risks.

Reporting Audit Findings

Communicating audit results is a central responsibility in internal auditing. Candidates must understand how to present findings clearly, objectively, and persuasively. Reports should summarize key risks, highlight control deficiencies, and provide practical recommendations for improvement.

Auditors must tailor communication to the audience, ensuring that management and governance bodies understand the implications of audit findings. Clear reporting supports informed decision-making, drives corrective actions, and reinforces the credibility of the internal audit function.

Monitoring Implementation of Recommendations

Follow-up activities ensure that audit recommendations are effectively implemented and risks are mitigated. Candidates must understand how to track corrective actions, assess their effectiveness, and report progress to management and oversight committees.

Monitoring supports accountability, reinforces risk management practices, and contributes to organizational improvement. Auditors must evaluate whether actions taken address identified weaknesses and achieve intended outcomes, providing assurance that audit efforts deliver lasting value.

Understanding Cognitive Requirements

CIA Part 2 evaluates candidates at both basic and proficient cognitive levels. Basic-level questions assess knowledge recall and comprehension of fundamental concepts and procedures. Proficient-level questions require the application of knowledge, analysis, evaluation, and formulation of recommendations based on criteria.

Candidates must integrate theoretical knowledge with practical application, demonstrating the ability to assess complex scenarios, interpret findings, and provide actionable advice. Mastery of both cognitive levels ensures readiness to perform professional audit tasks competently.

Scenario-Based Analysis

Scenario-based questions simulate real-world audit challenges, requiring candidates to analyze situations, identify risks, evaluate controls, and recommend solutions. CIA Part 2 emphasizes applying judgment and professional standards to realistic scenarios, testing critical thinking and decision-making skills.

Candidates must synthesize information from multiple sources, prioritize areas of concern, and select appropriate audit procedures. Effective scenario analysis demonstrates the ability to apply theoretical concepts in practical contexts, providing insights that support organizational objectives.

Applying Professional Standards

Knowledge of professional internal auditing standards is essential for conducting effective audits. CIA Part 2 tests candidates on their ability to apply standards in planning engagements, collecting evidence, reporting findings, and monitoring corrective actions.

Adherence to standards ensures consistency, reliability, and ethical integrity in audit activities. Candidates must integrate standards with judgment to evaluate processes, interpret results, and provide recommendations that enhance organizational performance.

Leveraging Technology in Auditing

Technology plays an important role in modern auditing practices. Candidates should understand how tools such as data analytics, automated testing, and continuous monitoring can enhance audit efficiency and effectiveness.

Technology enables auditors to analyze large datasets, identify patterns, detect anomalies, and improve the accuracy of findings. Candidates must demonstrate the ability to integrate technological outputs into audit conclusions and use technology to support evidence-based recommendations.

Risk Assessment and Control Prioritization

Assessing risk is fundamental to prioritizing audit engagements. Candidates must evaluate the likelihood and impact of potential risks, focusing efforts on areas with the highest significance. CIA Part 2 emphasizes the integration of risk assessment with control evaluation to ensure audits address the most critical organizational concerns.

Effective prioritization allows auditors to allocate resources efficiently, focus on high-impact areas, and provide management with insights that support strategic decision-making. Understanding the interaction between risk and controls is essential for effective audit planning and execution.

Enhancing Operational Efficiency

Auditors play a vital role in improving operational effectiveness by identifying inefficiencies, evaluating processes, and recommending enhancements. CIA Part 2 requires candidates to understand how audit activities can streamline operations, strengthen controls, and support organizational goals.

Evaluating processes, assessing workflows, and recommending improvements help organizations achieve objectives more efficiently. Audit insights contribute to cost reduction, risk mitigation, and enhanced overall performance.

Professional Judgment in Internal Auditing

Applying professional judgment is critical throughout the audit process. Candidates must demonstrate the ability to make informed decisions regarding planning, evidence evaluation, risk assessment, and reporting.

Judgment is required to interpret complex situations, balance priorities, and determine the most effective audit procedures. Strong judgment skills ensure that recommendations are practical, actionable, and aligned with organizational needs.

Preparing for Proficient-Level Topics

Proficient-level topics in CIA Part 2 involve higher-order thinking, including analysis, evaluation, and synthesis. Candidates must assess complex processes, evaluate the effectiveness of controls, and formulate actionable recommendations.

Preparation for these topics involves scenario-based practice, application of professional standards, and critical evaluation of audit processes. Mastery of proficient-level concepts equips candidates to handle real-world auditing challenges effectively.

Study Techniques and Exam Preparation

Successful preparation for CIA Part 2 requires structured study, consistent review, and practical application of knowledge. Candidates should allocate sufficient time to understand internal audit practices, professional standards, and engagement procedures.

Practice exercises, case studies, and scenario-based questions help reinforce learning, improve analytical skills, and enhance problem-solving abilities. Regular self-assessment ensures that candidates can apply concepts accurately and confidently during the exam.

Time Management Strategies

Managing time effectively during the exam is crucial for completing all questions. Candidates must practice reading scenarios, analyzing data, and selecting appropriate responses efficiently. Timed practice helps build accuracy, confidence, and stamina for answering multiple-choice questions within the allotted period.

Strategic preparation involves identifying areas of strength and weakness, focusing on topics that require improvement, and practicing practical applications to reinforce understanding. Effective time management enhances performance and ensures readiness for exam conditions.

Continuous Professional Development

Continuous learning and professional development are essential for internal auditors. CIA Part 2 emphasizes the importance of staying current with evolving audit practices, standards, and emerging technologies.

Auditors must adapt to organizational changes, regulatory updates, and new operational risks. Continuous development ensures that audit activities remain relevant, effective, and aligned with best practices. Candidates who commit to ongoing learning strengthen their ability to perform audits competently and provide valuable insights.

Integrating Theory and Practice

CIA Part 2 tests candidates on the ability to apply theoretical knowledge in practical audit situations. This includes planning and executing engagements, evaluating controls, analyzing data, and providing actionable recommendations.

Integrating theory with practice develops critical thinking, decision-making, and problem-solving skills. Candidates must synthesize information, apply professional standards, and deliver findings that support organizational improvement and risk management objectives.

Reporting and Follow-Up Best Practices

Effective reporting and follow-up are essential for ensuring that audit recommendations are implemented and risks are mitigated. Candidates must understand how to track corrective actions, assess their impact, and communicate progress to management and governance bodies.

Prioritizing recommendations, presenting evidence logically, and monitoring implementation reinforce accountability and demonstrate the value of the audit function. Follow-up ensures that audit activities result in meaningful and lasting improvements.

Strategic Value of Internal Auditing

Internal auditing provides strategic insights into organizational performance, risk management, and governance. CIA Part 2 emphasizes understanding how audit activities influence decision-making, improve operational efficiency, and strengthen control environments.

Candidates must recognize the broader organizational context, ensuring that audit engagements support strategic objectives and contribute to continuous improvement. This perspective enables auditors to provide recommendations that enhance overall organizational effectiveness.

CIA Part 2 evaluates the practical application of internal auditing, including planning, performing, and reporting engagements. The exam tests both basic and proficient knowledge, emphasizing professional standards, risk assessment, analytical skills, and judgment.

Candidates who integrate theoretical knowledge with practical application, maintain audit quality, and demonstrate professional judgment are well-prepared to succeed in CIA Part 2 and contribute effectively to internal audit functions.

Planning and Managing Audit Engagements

Planning is a critical component of CIA Part 2. Candidates must understand how to define audit objectives, determine the scope, and allocate resources appropriately. Effective planning involves identifying high-risk areas, establishing priorities, and selecting suitable audit techniques.

Managing the internal audit activity requires overseeing engagements, coordinating team efforts, and ensuring compliance with professional standards. Candidates must demonstrate the ability to anticipate potential challenges, allocate resources efficiently, and maintain clear communication with stakeholders. Proper management ensures audit activities are aligned with organizational priorities and objectives.

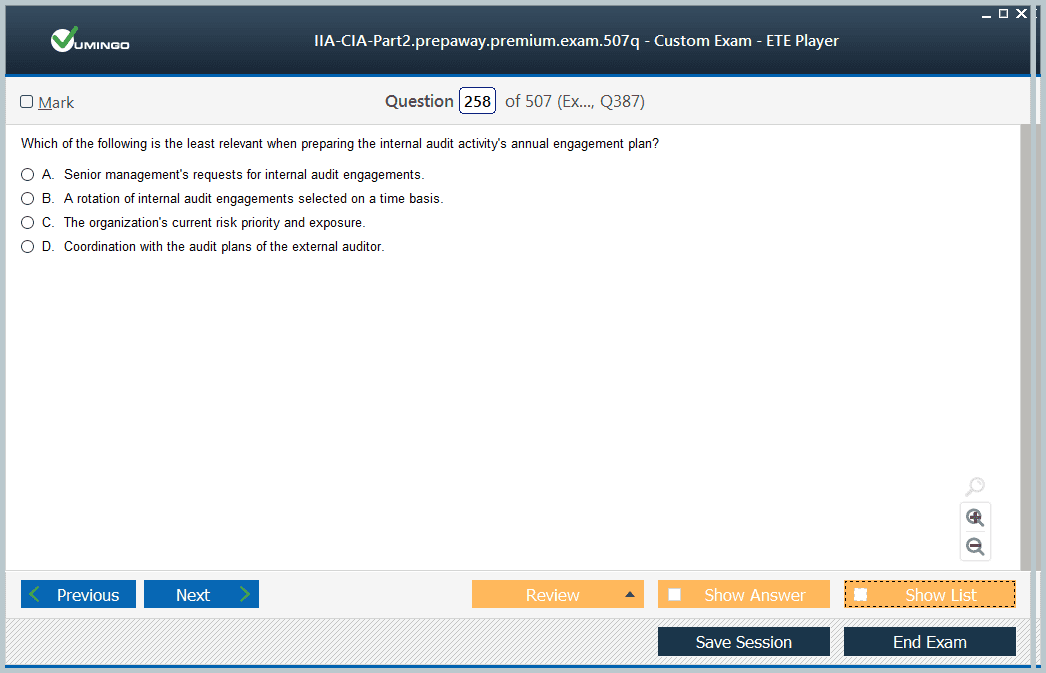

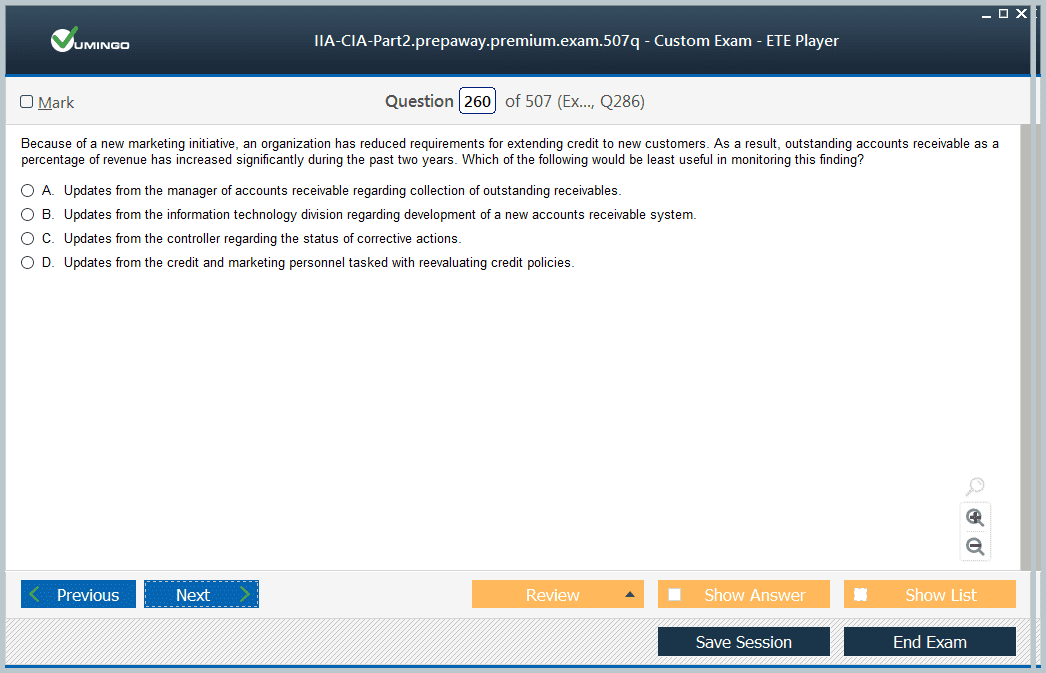

Conducting Engagements

Performing audit engagements involves collecting and analyzing evidence to evaluate organizational processes and controls. Candidates must understand methods for obtaining reliable evidence, including document reviews, observations, interviews, and data analysis.

Analyzing evidence requires critical thinking and the ability to assess relevance and reliability. Candidates must identify operational inefficiencies, control gaps, and risk exposures. Effective evaluation allows auditors to provide recommendations that enhance processes, mitigate risks, and support governance.

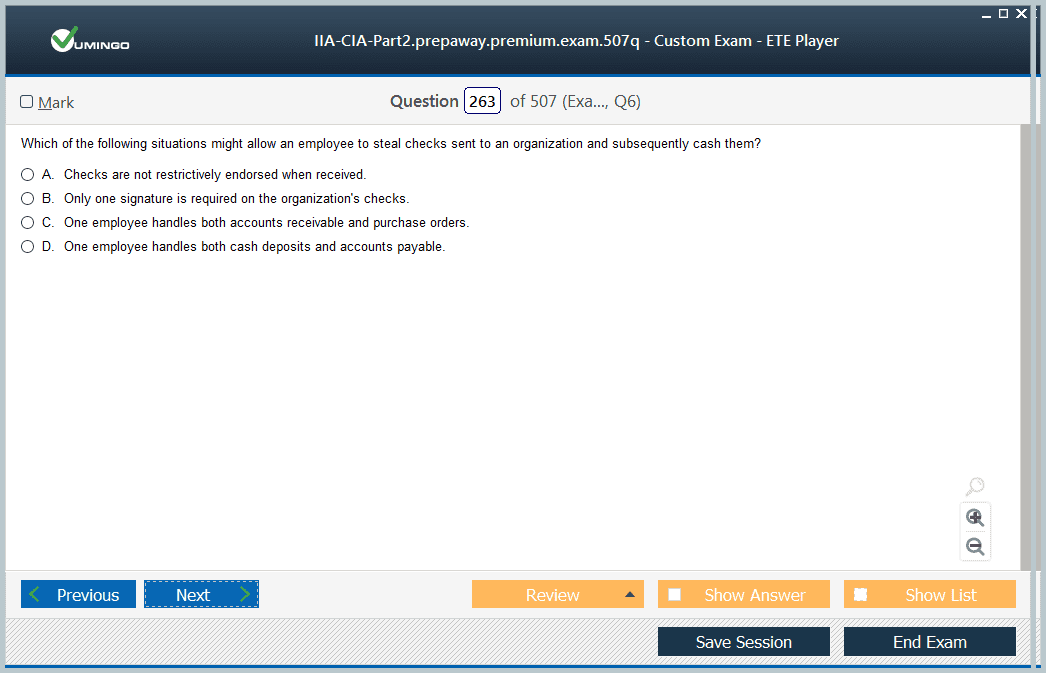

Control Assessment and Risk Evaluation

Control assessment is central to CIA Part 2. Candidates must evaluate whether internal controls are effectively designed and operating as intended. This includes assessing financial, operational, and compliance processes to detect weaknesses or deficiencies.

Risk evaluation involves identifying potential threats, prioritizing areas based on significance, and integrating risk considerations into audit planning. Candidates must apply risk-based approaches to ensure that audit engagements focus on areas with the greatest impact on organizational objectives.

Analytical Procedures and Data Interpretation

Analytical procedures play a key role in auditing by helping identify trends, anomalies, and deviations. CIA Part 2 tests candidates on their ability to analyze data, interpret results, and draw meaningful conclusions.

Candidates must compare actual performance to benchmarks, investigate discrepancies, and assess the implications for organizational processes. Analytical skills enable auditors to focus on critical areas, allocate resources effectively, and provide recommendations grounded in evidence.

Reporting and Communication of Findings

Effective reporting is essential in internal auditing. Candidates must demonstrate the ability to communicate findings clearly, concisely, and persuasively. Reports should summarize risks, highlight control deficiencies, and provide actionable recommendations.

Communication involves presenting information in a structured manner, prioritizing key issues, and tailoring content to different stakeholders. Clear reporting ensures that management and oversight bodies understand the implications of audit results and can take appropriate corrective actions.

Follow-Up and Monitoring

Follow-up ensures that audit recommendations are implemented and risks are addressed. Candidates must understand how to track corrective actions, evaluate their effectiveness, and report progress to management.

Monitoring reinforces accountability, supports risk mitigation, and contributes to organizational improvement. Auditors must assess whether corrective measures adequately address identified risks and whether additional actions are necessary to strengthen controls and processes.

Cognitive Levels and Exam Focus

CIA Part 2 evaluates knowledge at basic and proficient levels. Basic-level questions assess comprehension of fundamental concepts and procedures, while proficient-level questions test the ability to apply knowledge, analyze scenarios, evaluate information, and make informed judgments.

Candidates must integrate knowledge from multiple areas, apply professional standards, and demonstrate decision-making skills. Mastery of both cognitive levels is essential for performing professional auditing tasks competently.

Scenario-Based Application

Scenario-based questions simulate real-world auditing challenges. Candidates must analyze situations, identify risks, evaluate controls, and provide practical recommendations. CIA Part 2 emphasizes the ability to apply judgment and professional standards to realistic audit scenarios.

Effective scenario analysis requires synthesizing information, prioritizing risks, and selecting appropriate audit procedures. Candidates must demonstrate the ability to interpret scenarios accurately and apply standards to produce actionable insights.

Professional Standards and Ethics

Knowledge and application of professional standards are critical in CIA Part 2. Candidates must understand standards related to audit planning, evidence collection, reporting, and follow-up. Applying these standards ensures audits are conducted systematically, ethically, and consistently.

Ethical considerations guide auditors in evaluating processes objectively, communicating findings transparently, and maintaining professional integrity. Adherence to standards enhances audit credibility and strengthens organizational governance.

Leveraging Technology in Auditing

Technology is increasingly important in auditing. Candidates should understand how tools such as data analytics, automated testing, and continuous monitoring enhance audit efficiency and effectiveness.

Technology enables auditors to process large volumes of data, identify patterns, detect anomalies, and improve the accuracy of findings. Candidates must demonstrate the ability to interpret technological outputs and integrate them into audit conclusions and recommendations.

Risk Assessment and Prioritization

Assessing and prioritizing risks is fundamental to effective auditing. Candidates must evaluate the likelihood and impact of potential risks and focus audit efforts on the areas of greatest significance. CIA Part 2 emphasizes risk-based planning to ensure that engagements address the most critical organizational concerns.

Effective risk prioritization allows auditors to allocate resources efficiently, identify areas of vulnerability, and provide management with insights that support strategic decision-making. Understanding the interplay between risk and controls is key to successful audit outcomes.

Enhancing Organizational Efficiency

Auditors contribute to operational improvement by evaluating processes, identifying inefficiencies, and recommending enhancements. CIA Part 2 requires candidates to understand how audits can optimize workflows, strengthen controls, and support organizational goals.

Evaluating processes, assessing performance metrics, and proposing improvements help organizations achieve objectives efficiently. Audit insights contribute to cost reduction, risk mitigation, and enhanced operational performance.

Professional Judgment and Decision-Making

Professional judgment is critical in all stages of auditing, from planning to reporting. Candidates must demonstrate the ability to make informed decisions based on evidence, standards, and organizational objectives.

Judgment is applied to evaluate complex situations, select appropriate audit procedures, and balance competing priorities. Effective judgment ensures that audit recommendations are practical, actionable, and aligned with organizational needs.

Proficient-Level Preparation

Proficient-level topics involve higher-order thinking, including analysis, evaluation, and synthesis. Candidates must assess complex processes, evaluate the effectiveness of controls, and formulate actionable recommendations.

Preparation involves scenario-based practice, application of standards, and critical evaluation of audit processes. Mastery of proficient-level content ensures candidates can handle real-world auditing challenges effectively.

Study Strategies for CIA Part 2

Successful preparation requires structured study, consistent review, and practical application of knowledge. Candidates should allocate sufficient time to understand internal audit practices, professional standards, and engagement processes.

Practice exercises, case studies, and scenario-based questions reinforce learning, develop analytical skills, and improve problem-solving abilities. Regular self-assessment helps candidates gauge readiness and apply concepts confidently during the exam.

Time Management During the Exam

Completing the exam within the allocated time is crucial. Candidates must practice reading scenarios, analyzing data, and selecting answers efficiently. Timed practice helps build accuracy, confidence, and stamina for answering all multiple-choice questions.

Strategic exam preparation involves identifying areas of strength and weakness, focusing on topics requiring improvement, and practicing practical applications to reinforce understanding. Effective time management is key to achieving optimal performance.

Continuous Professional Development

Continuous learning is essential for internal auditors. CIA Part 2 emphasizes staying current with auditing practices, emerging technologies, and evolving standards.

Auditors must adapt to organizational changes, regulatory updates, and new risk environments. Continuous professional development ensures audit activities remain relevant, effective, and aligned with best practices.

Practical Application and Integration

CIA Part 2 requires candidates to apply theoretical knowledge in practical auditing scenarios. This includes planning engagements, evaluating controls, analyzing data, and providing actionable recommendations.

Integrating theory and practice develops critical thinking, decision-making, and problem-solving skills. Candidates must synthesize information, apply standards, and deliver findings that support risk management and organizational improvement.

Reporting and Follow-Up Practices

Effective reporting and follow-up ensure audit recommendations are implemented and risks mitigated. Candidates must track corrective actions, assess their impact, and communicate progress to management.

Prioritizing recommendations, presenting evidence logically, and monitoring implementation reinforce accountability and demonstrate the value of internal audit functions. Follow-up ensures that audit activities have lasting organizational impact.

Strategic Importance of Internal Auditing

Internal auditing provides strategic insights into governance, risk management, and operational effectiveness. CIA Part 2 emphasizes understanding how audit engagements influence organizational decision-making and improve processes.

Candidates must recognize the broader organizational context, ensuring audits align with strategic objectives and support continuous improvement. This perspective enables auditors to deliver recommendations that enhance performance and strengthen governanc

Conclusion

CIA Part 2 evaluates the application of internal auditing concepts, including planning, performing, and reporting engagements. The exam tests both basic and proficient knowledge, focusing on risk assessment, analytical skills, professional judgment, and adherence to standards.

Candidates who integrate theoretical knowledge with practical application, maintain audit quality, and demonstrate judgment are well-prepared to succeed in CIA Part 2 and contribute effectively to internal audit functions.

IIA IIA-CIA-Part2 practice test questions and answers, training course, study guide are uploaded in ETE Files format by real users. Study and Pass IIA-CIA-Part2 Certified Internal Auditor - Part 2, Practice of Internal Auditing certification exam dumps & practice test questions and answers are to help students.

- IIA-CIA-Part1 - CIA Part 1 - Essentials of Internal Auditing

- IIA-CIA-Part2 - Certified Internal Auditor - Part 2, Practice of Internal Auditing

- IIA-CIA-Part3 - Certified Internal Auditor - Part 3, Business Analysis and Information Technology

- CIA-Part2-2025 - CIA Part 2 - Internal Audit Engagement

- IIA-CHAL-QISA - Qualified Info Systems Auditor CIA Challenge

- CIA-Part1-2025 - CIA Part 1 - Internal Audit Fundamentals

Purchase IIA-CIA-Part2 Exam Training Products Individually

Why customers love us?

What do our customers say?

The resources provided for the IIA certification exam were exceptional. The exam dumps and video courses offered clear and concise explanations of each topic. I felt thoroughly prepared for the IIA-CIA-Part2 test and passed with ease.

Studying for the IIA certification exam was a breeze with the comprehensive materials from this site. The detailed study guides and accurate exam dumps helped me understand every concept. I aced the IIA-CIA-Part2 exam on my first try!

I was impressed with the quality of the IIA-CIA-Part2 preparation materials for the IIA certification exam. The video courses were engaging, and the study guides covered all the essential topics. These resources made a significant difference in my study routine and overall performance. I went into the exam feeling confident and well-prepared.

The IIA-CIA-Part2 materials for the IIA certification exam were invaluable. They provided detailed, concise explanations for each topic, helping me grasp the entire syllabus. After studying with these resources, I was able to tackle the final test questions confidently and successfully.

Thanks to the comprehensive study guides and video courses, I aced the IIA-CIA-Part2 exam. The exam dumps were spot on and helped me understand the types of questions to expect. The certification exam was much less intimidating thanks to their excellent prep materials. So, I highly recommend their services for anyone preparing for this certification exam.

Achieving my IIA certification was a seamless experience. The detailed study guide and practice questions ensured I was fully prepared for IIA-CIA-Part2. The customer support was responsive and helpful throughout my journey. Highly recommend their services for anyone preparing for their certification test.

I couldn't be happier with my certification results! The study materials were comprehensive and easy to understand, making my preparation for the IIA-CIA-Part2 stress-free. Using these resources, I was able to pass my exam on the first attempt. They are a must-have for anyone serious about advancing their career.

The practice exams were incredibly helpful in familiarizing me with the actual test format. I felt confident and well-prepared going into my IIA-CIA-Part2 certification exam. The support and guidance provided were top-notch. I couldn't have obtained my IIA certification without these amazing tools!

The materials provided for the IIA-CIA-Part2 were comprehensive and very well-structured. The practice tests were particularly useful in building my confidence and understanding the exam format. After using these materials, I felt well-prepared and was able to solve all the questions on the final test with ease. Passing the certification exam was a huge relief! I feel much more competent in my role. Thank you!

The certification prep was excellent. The content was up-to-date and aligned perfectly with the exam requirements. I appreciated the clear explanations and real-world examples that made complex topics easier to grasp. I passed IIA-CIA-Part2 successfully. It was a game-changer for my career in IT!