- Home

- FINRA Certifications

- Series 7 General Securities Representative Qualification Examination (GS) Dumps

Pass FINRA Series 7 Exam in First Attempt Guaranteed!

Get 100% Latest Exam Questions, Accurate & Verified Answers to Pass the Actual Exam!

30 Days Free Updates, Instant Download!

Series 7 Premium Bundle

- Premium File 400 Questions & Answers. Last update: Jun 26, 2026

- Training Course 13 Video Lectures

- Study Guide 541 Pages

Last Week Results!

Includes question types found on the actual exam such as drag and drop, simulation, type-in and fill-in-the-blank.

Based on real-life scenarios similar to those encountered in the exam, allowing you to learn by working with real equipment.

Developed by IT experts who have passed the exam in the past. Covers in-depth knowledge required for exam preparation.

All FINRA Series 7 certification exam dumps, study guide, training courses are Prepared by industry experts. PrepAway's ETE files povide the Series 7 General Securities Representative Qualification Examination (GS) practice test questions and answers & exam dumps, study guide and training courses help you study and pass hassle-free!

The FINRA Series 7 Exam: Key Insights for Future Financial Representatives

The FINRA Series 7 exam, formally known as the General Securities Representative Exam, is one of the most recognized licensing requirements in the American financial services industry. It is administered by the Financial Industry Regulatory Authority, commonly known as FINRA, and is required for individuals who want to buy and sell a broad range of securities products on behalf of clients. Passing this exam grants a candidate the legal authorization to work as a registered representative at a broker-dealer firm, making it a critical milestone for anyone entering the securities profession.

The exam covers an extensive range of topics, from equity and debt securities to options, mutual funds, retirement accounts, and regulatory requirements. It is not a general knowledge test but a rigorous assessment of whether a candidate can competently perform the duties of a general securities representative. FINRA designed the exam to ensure that only individuals with a thorough and verified understanding of financial products, client suitability, and industry regulations are permitted to advise clients and execute transactions in the marketplace.

The Regulatory Body That Oversees the Exam

FINRA is a nonprofit organization authorized by Congress to oversee broker-dealers and their registered representatives in the United States. It operates under the supervision of the Securities and Exchange Commission and functions as a self-regulatory organization for the brokerage industry. FINRA's mission is to protect investors and ensure that the securities markets operate fairly and honestly, and its licensing exams are a core tool for achieving that mission.

Every person who works as a securities representative at a FINRA-member firm must meet licensing requirements set by the organization. The Series 7 is the central credential in that framework. FINRA regularly reviews and updates the exam to ensure it reflects current market practices, regulatory changes, and the evolving responsibilities of registered representatives. This ongoing commitment to relevance is one reason the Series 7 continues to carry such weight with employers and regulators alike.

Structure and Format of the Examination

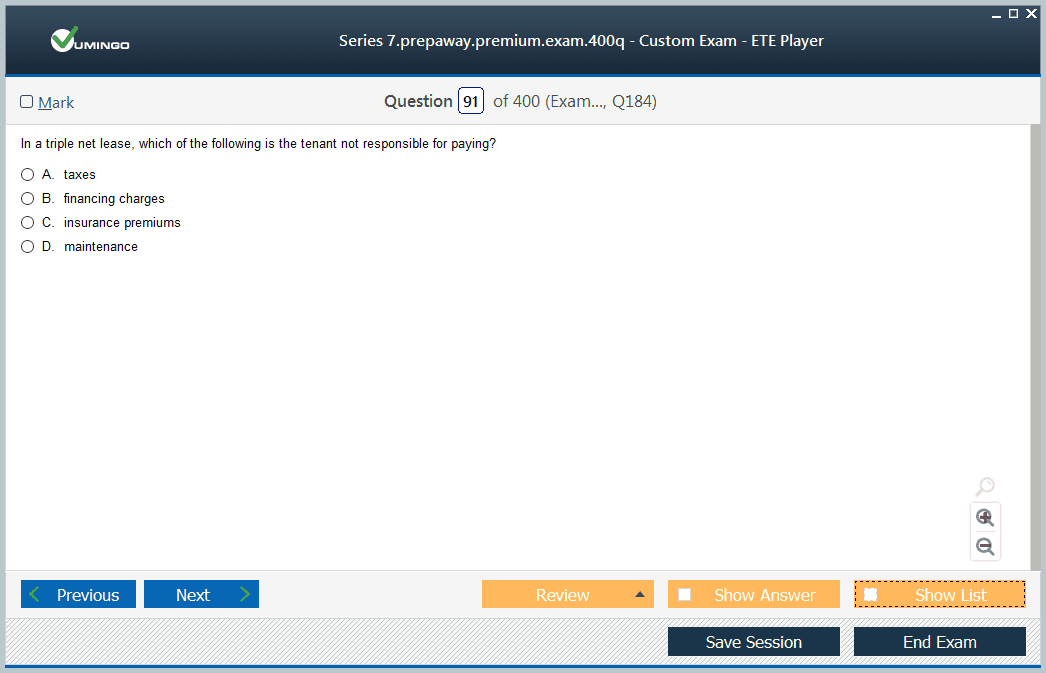

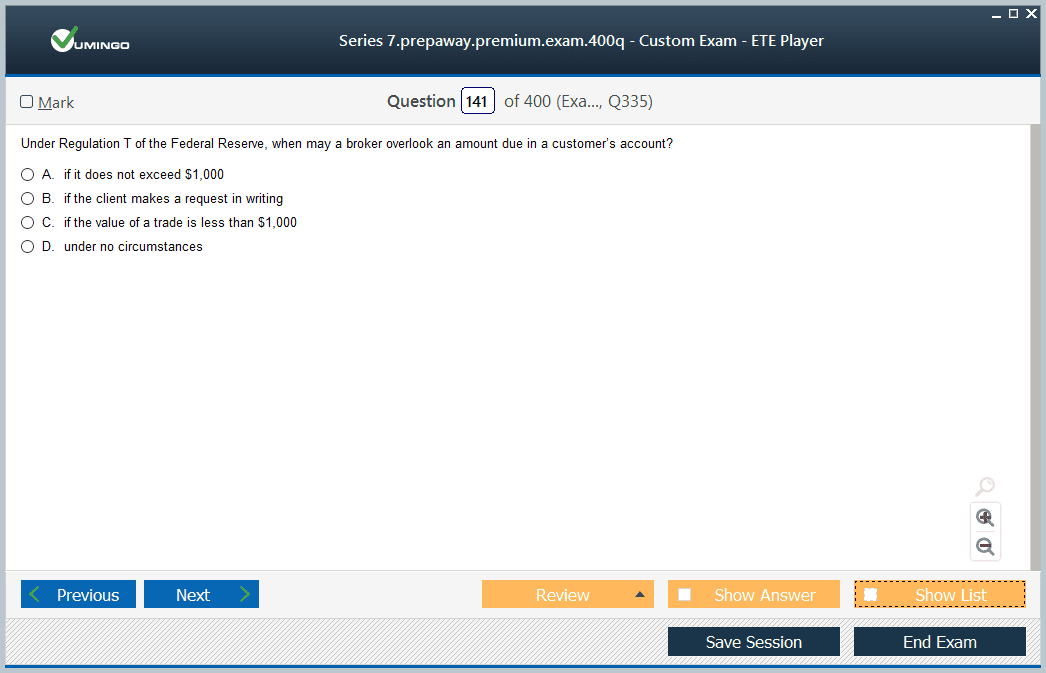

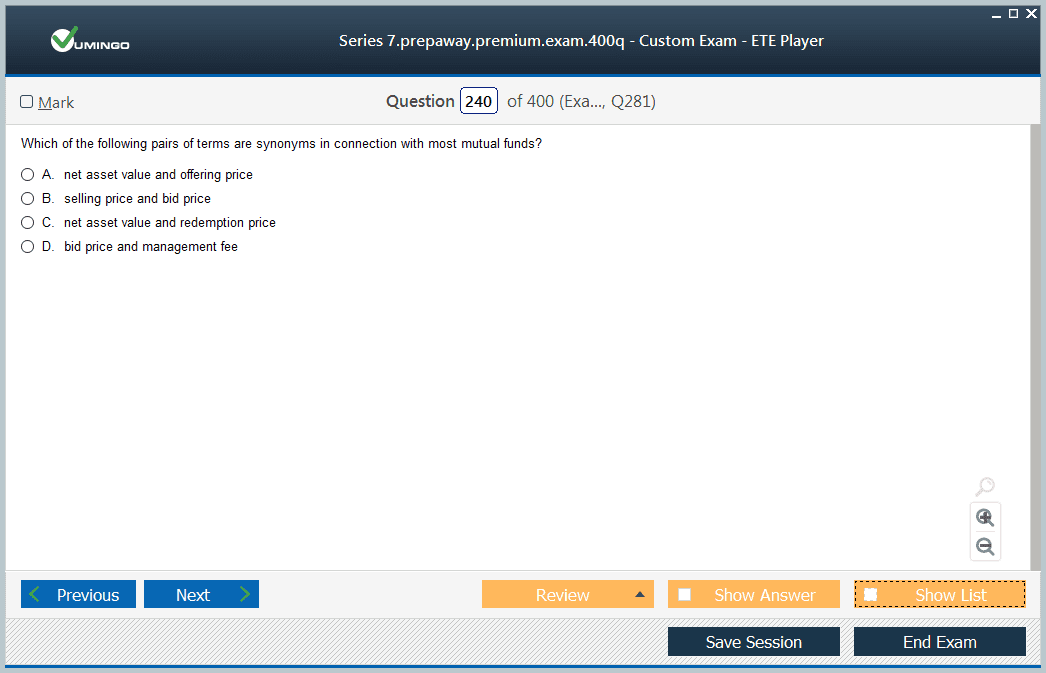

The Series 7 exam consists of 125 scored questions, with an additional 10 unscored pilot questions embedded throughout the exam that candidates cannot identify. The total time allotted is 225 minutes, giving candidates approximately one minute and forty-five seconds per question on average. All questions are in multiple choice format, each presenting four answer choices with one correct response. The passing score is 72 percent, meaning a candidate must answer at least 90 of the 125 scored questions correctly.

The exam is divided into four major job function areas: seeks business for the broker-dealer through customers and potential customers; opens accounts after obtaining and evaluating customers' financial profile and investment objectives; provides customers with information about investments, makes suitable recommendations, transfers assets, and maintains appropriate records; and obtains and verifies customers' purchase and sale instructions and agreements, processes, completes, and confirms transactions. Each of these areas carries a different weight in terms of the number of questions it contributes to the overall exam, with some sections demanding more attention during preparation than others.

Prerequisites Candidates Must Satisfy Before Registration

Unlike some professional exams that allow anyone to register independently, the Series 7 requires a sponsoring FINRA-member firm. A candidate cannot simply sign up for the exam on their own initiative. They must first be employed by or associated with a broker-dealer that is a member of FINRA, and that firm must submit the candidate's registration through FINRA's Central Registration Depository system. This requirement ensures that candidates are taking the exam with a real professional purpose rather than out of casual curiosity.

In addition to firm sponsorship, candidates must pass the Securities Industry Essentials exam, commonly called the SIE, before or alongside registering for the Series 7. The SIE is a co-requisite that tests foundational knowledge of the securities industry and can be taken without firm sponsorship. Most candidates take the SIE first to build their baseline knowledge before pursuing the more demanding Series 7. Together, the two exams form a comprehensive gateway into the registered representative role, and neither alone is sufficient to obtain full licensure.

Topics That Demand the Most Attention During Study

Among the many subjects covered on the Series 7 exam, options are widely regarded as one of the most challenging and heavily tested areas. Options involve complex strategies that include calls, puts, combinations, spreads, and hedging techniques, all of which require candidates to calculate potential gains, losses, breakeven points, and maximum risk scenarios. Many test-takers report spending more time on options than on any other single topic, and for good reason: the exam devotes a significant portion of its questions to this area.

Equity securities, debt instruments, and mutual funds also receive substantial coverage on the exam. Candidates must be comfortable with the characteristics of common and preferred stock, the mechanics of bond pricing and yield calculations, the structure and taxation of various fund types, and the regulatory requirements governing how these products are sold to clients. Suitability is a recurring theme across all product categories, as the exam consistently tests whether candidates can match the right investment to the right client based on financial circumstances, risk tolerance, and investment objectives.

How Suitability Rules Shape Exam Content

Suitability is one of the most foundational concepts in the Series 7 curriculum and appears throughout the exam in various forms. FINRA requires registered representatives to have a reasonable basis for believing that a recommended transaction or investment strategy is suitable for a customer based on information obtained through reasonable diligence. This means candidates must know how to evaluate a client's financial situation, investment experience, risk tolerance, time horizon, and specific needs before making any recommendation.

The regulatory framework around suitability was significantly strengthened with the adoption of Regulation Best Interest, which went into effect in 2020 and raised the standard for broker-dealers when making recommendations to retail customers. The Series 7 exam now includes content related to this regulation, testing whether candidates understand the heightened obligations it imposes. Candidates who grasp suitability not just as a rule to memorize but as a genuine professional responsibility tend to perform better on the exam because suitability logic ties together many different question types across product categories.

Preparation Timelines and Study Approaches That Succeed

Most candidates spend between 80 and 150 hours preparing for the Series 7, though the actual time needed varies significantly based on prior knowledge and professional background. Someone who has worked in a financial services role for several years may need fewer hours than someone entering directly from an unrelated field. Regardless of background, a structured study plan that allocates time to each exam domain in proportion to its weight on the actual exam tends to produce better results than unfocused reading.

Practice exams are one of the most effective preparation tools available. Taking full-length timed practice tests under realistic conditions helps candidates identify weak areas, build endurance for the lengthy exam, and become comfortable with the specific way FINRA phrases its questions. Many successful candidates report taking dozens of practice exams over the course of their preparation. Review courses from providers like Kaplan Financial Education, Securities Institute of America, and Pass Perfect offer structured curricula, video lessons, and question banks that give candidates a comprehensive preparation framework.

The Role of the SIE Exam as a Foundation

The Securities Industry Essentials exam plays an important role in preparing candidates for the Series 7 by establishing baseline knowledge of the securities industry before the more demanding content of the Series 7 is introduced. The SIE covers topics like types of securities products, how markets work, regulatory agencies and their functions, and prohibited practices. While these subjects are covered at a higher level in the SIE than in the Series 7, building familiarity with them first makes the deeper Series 7 content more approachable.

One strategic advantage of the SIE is that it can be passed and held for four years while a candidate seeks firm sponsorship and registers for the Series 7. This allows individuals who are not yet employed at a broker-dealer to begin the licensing process, demonstrate initiative to potential employers, and enter the job market with one exam already completed. Many career counselors in the financial services industry recommend this approach, as having a passed SIE on a resume signals genuine commitment to the profession and gives a candidate a competitive edge during the hiring process.

Career Opportunities That Open After Passing

Earning a Series 7 license opens doors to a wide range of roles within the financial services industry. The most direct path is becoming a registered representative, also called a stockbroker or financial advisor, at a brokerage firm where the primary responsibilities include managing client accounts, making investment recommendations, and executing trades. These roles exist at major wirehouses like Merrill Lynch, Morgan Stanley, and Wells Fargo Advisors, as well as at regional broker-dealers and independent firms.

Beyond the traditional brokerage role, a Series 7 license is often required or preferred for positions in investment banking, financial planning, institutional sales, and trading. Many compliance officers, operations professionals, and branch managers at securities firms also hold the Series 7 as part of their broader professional qualifications. For candidates who go on to pursue additional licenses such as the Series 63, Series 65, or Series 24, the Series 7 serves as the foundational credential that the rest of the licensing framework builds upon.

How Compensation Relates to Licensure

Holding a Series 7 license has a direct and measurable impact on compensation potential in the financial services industry. Registered representatives typically earn income through a combination of salary, commissions, and bonuses, with the commission component tied directly to the transactions and products they are licensed to sell. Because the Series 7 grants authorization to sell the broadest range of securities products, representatives who hold this license have the widest possible earning potential compared to those holding more limited licenses.

According to industry salary data, registered representatives with a Series 7 license earn salaries that range from modest starting figures at smaller firms to very substantial incomes at major financial institutions, particularly as they build client books and accumulate assets under management. Many experienced representatives in high-production roles earn well into six figures annually. This compensation potential is one of the primary drivers of demand for the Series 7 among individuals entering the financial services industry, and it reflects the significant responsibilities and professional standards that the license imposes.

Exam Day Logistics and What to Anticipate

Candidates take the Series 7 exam at Prometric testing centers, which are located throughout the United States and in many international locations. Registration is managed through FINRA's system, and once a candidate's firm submits the registration, the candidate receives instructions for scheduling at a Prometric location. The exam environment is controlled and secure, with strict identity verification procedures, prohibited items policies, and continuous monitoring throughout the testing session.

On exam day, candidates should arrive early, bring accepted forms of identification, and be prepared to leave all personal items outside the testing room. The exam interface is computer-based, and candidates are given scratch paper or an erasable notepad for calculations. The lengthy time block of three hours and forty-five minutes can be mentally taxing, so candidates benefit from practicing endurance during their preparation by completing full-length timed practice exams. Knowing what to expect on exam day reduces anxiety and allows candidates to perform at their best when it matters most.

Consequences of Failing and Retake Policies

Not every candidate passes the Series 7 on the first attempt, and FINRA has established a clear retake policy for those who do not achieve the required score. After a failed attempt, candidates must wait 30 days before retaking the exam. If a candidate fails a second time, the same 30-day waiting period applies. Following a third failed attempt, however, candidates must wait 180 days before they can sit for the exam again. This escalating waiting period is designed to encourage thorough preparation rather than repeated attempts without meaningful study between sittings.

Failing the exam does not disqualify a candidate from the profession, but it does create delays that can affect employment timelines and put pressure on the relationship with the sponsoring firm. Many firms have internal policies about how many attempts they will support for an employee. Candidates who approach their preparation seriously, use quality study materials, and take full-length practice exams regularly are significantly less likely to need a retake. The investment in thorough preparation is always more efficient than the cost in time and confidence of an unsuccessful first attempt.

Ethical Obligations of Registered Representatives

The Series 7 exam tests not only product knowledge and calculation skills but also the ethical obligations that registered representatives must uphold in their professional conduct. FINRA rules, SEC regulations, and the standards of conduct established by the Municipal Securities Rulemaking Board collectively define the ethical framework within which registered representatives must operate. Candidates are expected to know these rules and be able to apply them to realistic client scenarios.

Prohibited practices covered on the exam include churning, which refers to excessive trading in a client's account to generate commissions; front-running, which involves trading for a firm's own account ahead of a client order; and making unsuitable recommendations regardless of client instruction. The exam also covers rules around communications with the public, the proper handling of customer complaints, and the obligations that representatives have when they become aware of potential misconduct. Ethics-related questions appear consistently throughout the exam and are treated with the same rigor as technical product knowledge questions.

How Technology Has Changed Exam Preparation

The way candidates prepare for the Series 7 has changed considerably with the expansion of online learning platforms and digital study tools. Where candidates once relied primarily on physical textbooks and classroom instruction, today's candidates have access to adaptive learning software, video lectures, mobile flashcard apps, and online question banks with thousands of practice questions. These tools allow for more personalized study experiences that can adjust to a candidate's specific strengths and weaknesses in real time.

Some platforms use artificial intelligence to identify patterns in a candidate's incorrect answers and prioritize review of those topics in subsequent study sessions. This data-driven approach to preparation is more efficient than simply rereading chapters and has contributed to higher pass rates among candidates who use these tools consistently. The availability of mobile study apps also means that candidates can make productive use of commute time, lunch breaks, and other otherwise idle moments throughout the day, compressing preparation timelines without sacrificing depth of knowledge.

Maintaining the License After It Is Earned

Passing the Series 7 is not the end of the licensing journey. Registered representatives must maintain their license through ongoing compliance with FINRA's continuing education requirements. The continuing education program consists of two components: the regulatory element and the firm element. The regulatory element requires representatives to complete computer-based training within 120 days of their second registration anniversary and every three years thereafter. This training covers regulatory, compliance, ethical, and sales practice standards.

The firm element requires broker-dealers to conduct annual training programs for their registered personnel that address the products, services, and regulatory requirements relevant to their specific business activities. Firms design these programs based on a needs analysis that considers the types of products sold, customer profiles, and any compliance issues identified during the preceding year. Together, the regulatory and firm elements of continuing education ensure that registered representatives remain current with industry standards and regulatory changes throughout their careers, rather than relying solely on the knowledge they held at the time they passed the exam.

Conclusion

The FINRA Series 7 exam stands as one of the most consequential professional milestones in the financial services industry. It is not simply an administrative requirement or a regulatory checkbox but a meaningful test of whether an individual is prepared to take on the serious responsibilities that come with advising clients and executing transactions in the securities markets. Earning this license signals to employers, clients, and regulators that a representative has the knowledge, competence, and professional awareness needed to operate ethically and effectively in one of the most consequential industries in the economy.

For individuals who are serious about building a career in financial services, the Series 7 is almost always an essential part of the path. It expands earning potential, broadens career options, and establishes a professional identity that is recognized across the industry. The process of preparing for the exam, while demanding, is itself a valuable educational experience that builds the kind of comprehensive financial knowledge that serves representatives well throughout their careers, not just on exam day.

What makes this credential particularly significant is the breadth of what it covers. A candidate who passes the Series 7 does not simply know how to sell stocks. They understand how debt instruments are priced, how options strategies are constructed, how retirement accounts are regulated, how client suitability is assessed, and how the regulatory framework that governs the entire industry operates. That breadth of knowledge is genuinely useful in day-to-day professional life and gives representatives a foundation they can continue building on as they pursue additional licenses and take on greater responsibilities.

The financial services industry is one that rewards preparation, persistence, and professional integrity, and the Series 7 exam reflects all three of those values. Candidates who approach the exam with genuine commitment, allocate sufficient time to preparation, use quality study resources, and take the ethical dimensions of the license seriously are well positioned not just to pass but to thrive in the profession that the license unlocks. The exam is a beginning, not an end, and the career possibilities it opens are limited only by the effort and ambition that each representative brings to their work.

For anyone standing at the threshold of a financial services career and weighing whether the investment in Series 7 preparation is worthwhile, the answer that emerges consistently from industry professionals, hiring managers, and career counselors is an unambiguous yes. The credential carries real weight, delivers real opportunities, and represents a real commitment to the profession that the market continues to recognize and reward year after year.

FINRA Series 7 practice test questions and answers, training course, study guide are uploaded in ETE Files format by real users. Study and Pass Series 7 General Securities Representative Qualification Examination (GS) certification exam dumps & practice test questions and answers are to help students.

Exam Comments * The most recent comment are on top

Purchase Series 7 Exam Training Products Individually

Why customers love us?

What do our customers say?

The resources provided for the FINRA certification exam were exceptional. The exam dumps and video courses offered clear and concise explanations of each topic. I felt thoroughly prepared for the Series 7 test and passed with ease.

Studying for the FINRA certification exam was a breeze with the comprehensive materials from this site. The detailed study guides and accurate exam dumps helped me understand every concept. I aced the Series 7 exam on my first try!

I was impressed with the quality of the Series 7 preparation materials for the FINRA certification exam. The video courses were engaging, and the study guides covered all the essential topics. These resources made a significant difference in my study routine and overall performance. I went into the exam feeling confident and well-prepared.

The Series 7 materials for the FINRA certification exam were invaluable. They provided detailed, concise explanations for each topic, helping me grasp the entire syllabus. After studying with these resources, I was able to tackle the final test questions confidently and successfully.

Thanks to the comprehensive study guides and video courses, I aced the Series 7 exam. The exam dumps were spot on and helped me understand the types of questions to expect. The certification exam was much less intimidating thanks to their excellent prep materials. So, I highly recommend their services for anyone preparing for this certification exam.

Achieving my FINRA certification was a seamless experience. The detailed study guide and practice questions ensured I was fully prepared for Series 7. The customer support was responsive and helpful throughout my journey. Highly recommend their services for anyone preparing for their certification test.

I couldn't be happier with my certification results! The study materials were comprehensive and easy to understand, making my preparation for the Series 7 stress-free. Using these resources, I was able to pass my exam on the first attempt. They are a must-have for anyone serious about advancing their career.

The practice exams were incredibly helpful in familiarizing me with the actual test format. I felt confident and well-prepared going into my Series 7 certification exam. The support and guidance provided were top-notch. I couldn't have obtained my FINRA certification without these amazing tools!

The materials provided for the Series 7 were comprehensive and very well-structured. The practice tests were particularly useful in building my confidence and understanding the exam format. After using these materials, I felt well-prepared and was able to solve all the questions on the final test with ease. Passing the certification exam was a huge relief! I feel much more competent in my role. Thank you!

The certification prep was excellent. The content was up-to-date and aligned perfectly with the exam requirements. I appreciated the clear explanations and real-world examples that made complex topics easier to grasp. I passed Series 7 successfully. It was a game-changer for my career in IT!